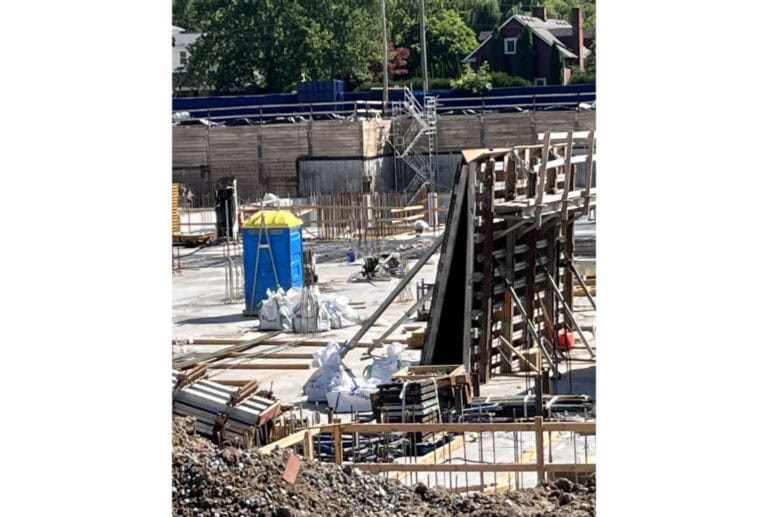

The chainsaws have been ripping through mature pines in Virgil. Councillors decided the score would be Developer 1 and Nature 0. In response, 700 trees are into the chipper so phase two of a housing project may proceed.

Locals argued against this, upset at the loss of habitat for birds and coyotes as a forest becomes another sea of roofs.

But they lost. Of course. Seems everybody wanting to create residential space lately is being greenlit. Bungalows in Virgil. Hulking condo towers in Glendale. Even a 41-unit beast lurking on the perimeter of Old Town. After all, who needs trees? Every time a member of council passes an open field or empty lot they must be aroused. Pave it, baby!

Well, time for a rethink. Especially now that Tariff Man’s in our lives.

A hefty number of properties currently for sale in the region are vacant. GTA real estate is far from the hot commodity it once was. Look at condos. Yikes. Eleven thousand resales available. Almost 17,000 new, unsold units up for grabs. Young owners trapped because prices have dropped 20 per cent since 2022 with buyers evaporating.

The home-building cartel calls it dire. “Despite a further Bank of Canada cut, excessive inventory and falling prices, GTA new home buyers are nowhere to be found,” says the Building Industry and Land Development Association (BILD).

And yet, we keep approving more, even though the price of new housing has been sticky and insane.

Does Virgil need 150 more families? Can the developer even flog that many new homes from plans and a sales trailer? Now that we’ve got a new wave of job-sucking Trump tariffs coming on April 2, was the Great Pine Slaughter a tad premature?

“I don’t see any immediate improvements in the housing market as we move into spring,” says Kymberley McKee, with Sotheby’s. “The economic uncertainty we’re facing will most likely pervade throughout the first half of the year, perhaps longer. Housing prices are still holding but they may begin to fall as 2025 progresses.”

She’s not alone in her caution.

“We’re back to swirling uncertainty,” adds Bosley’s Patrick Burke. “Given the housing market lives and dies on sentiment, the events of recent days will certainly complicate things. What nobody knows is how long the situation will be in place. Is it a short-lived few months of chaos or are tariffs here for the year and beyond? That’s the biggest question.”

The latest news isn’t house-friendly. The U.S. wants to address its $1.85 trillion annual deficit by gutting government (Elon has his own chainsaw) and getting the rest of the world to cough up tariff revenue for the privilege of selling to Americans. This will then enable Trump to fulfil his promise of cutting corporate taxes. On Elon, for example.

So what can we expect?

More rate cuts. Our guys will try to mitigate the tariff impact with cheaper mortgages. In a normal world, combined with those new 30-year loans and reduced downpayments, that would ignite a spring market. But not this time.

“My suggestion to buyers is don’t hesitate to make an offer reflecting what you trust is a fair price,” says McKee. “With offers few and far between, vendors are ready to negotiate.”

As for sellers, Burke says be realistic. “You need to dig into the reality of the market at the current time. We’re really in a ‘week by week’ market these days. Get dialed in on current conditions and make sure your pricing and overall strategy is backed up with facts.”

Or, you can be like Greg Sykes, over at Re/Max. If you like it, buy it. The Trump effect won’t last.

“Real estate has always been a foundational asset and people will always need a place to live, regardless of market conditions. If I may be so bold, I believe it is a good time to buy!”

But not to be a tree.